Bonuses paid by my employer

Profit-sharing |

Incentive plans |

Employer contribution |

Incentive plans and profit-sharing are two types of collective agreements that a company can implement:

Profit-sharing

Profit-sharing is a legal scheme that becomes mandatory when a company has more than 50 employees. It provides for the redistribution, in favour of employees, of a portion of the profits they have helped generate through their work. A share of profit-sharing is only paid out if the company makes a profit during the relevant financial year.

Incentive plans

Incentive plans are optional schemes that reflect the employer’s desire to financially involve employees in the company’s performance, based on objective criteria. These criteria might include, for example, improved results, increased productivity, enhanced customer service, and so on.

The payment and amount of the incentive bonus depend on achieving the objectives set out in the collective agreement signed between the company and its employee representatives. This agreement also defines how the incentive is distributed among employees.

Your employer pays out both profit-sharing and incentive bonuses before the first day of the sixth month following the end of the relevant financial year (for example, before 1 June if the financial year ends on 31 December).

You will then have the option to invest all or part of your bonuses into your savings plans.

Profit-sharing and incentive bonuses do not count towards the contribution limits for company savings plans (PEE) and collective retirement savings plans (PERCO), which are capped at 25 per cent of your gross annual salary.

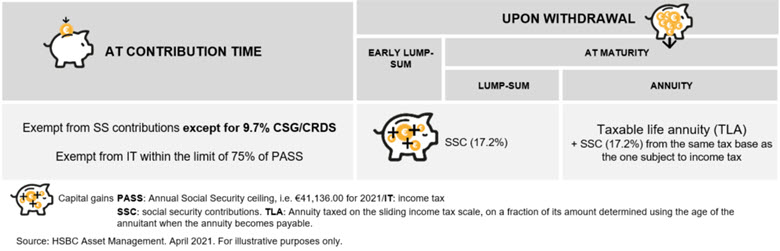

Taxation of incentives invested

Source: HSBC Asset Management. February 2026. For illustrative purposes only.

If you choose to collect your incentives instead, they’ll be subject to income tax.

Employer contribution

Employer matching contributions (abondement) are payments that an employer may choose to make to supplement employees’ voluntary savings in company savings plans.*

A set of rules defines how these contributions work:

- Which payments are eligible for matching contributions (sources or types of contributions, investment options),

- the matching rate (it cannot exceed 300 per cent of the employee’s contributions),

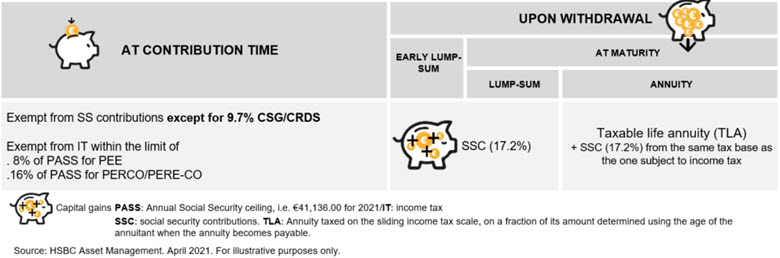

- the maximum limit (current regulatory ceilings: 8 per cent of the Annual Social Security Ceiling (PASS) for a company savings plan (PEE), and 16 per cent of the PASS for a collective or individual retirement savings plan (PERCO or PER))

*Note: Mandatory retirement savings plans (PER Obligatoire) are not eligible for employer matching contributions.

Taxation of employer contribution

Source: HSBC Asset Management. February 2026. For illustrative purposes only.