My project savings

Build up project savings with the Company Savings Plan (PEE).

Build up project savings with the Company Savings Plan (PEE).

Do you have a medium-term project in mind—such as buying a home, getting married, renovating, funding your children's education, or simply building up an emergency savings fund? Salary savings invested in your Company Savings Plan (PEE) for five years (except in cases of early withdrawal) can help you finance these goals under favourable conditions

The advantages of the company savings plan (PEE)

The advantages of the company savings plan (PEE)

|

A particularly favourable tax regime When you withdraw all or part of your savings, any capital gains are exempt from income tax and are only subject to the applicable social contributions. |

|

|

Your company helps you save |

|

|

Easy contributions

|

|

The PEE: A savings tool for everyone

To access a company savings plan (PEE), certain conditions apply :

- All employees within the same company are eligible

- Typically, you need at least three months of service to join

- Former employees who have retired or taken early retirement can continue making voluntary contributions (without employer matching), provided their plan remains open and they started contributing before leaving the company

Sources of funding

Accessing my savings

After this period, you can either withdraw your savings or keep them invested in the PEE.

However, you may request early withdrawal of all or part of your savings in certain situations, such as :

- Purchasing your main residence

- Marriage or civil partnerchip (PACS)

- Birth or adoption of a third child...

Learn more about early withdrawal options

Investing my savings

The amounts you contribute are invested in units of Company Investment Funds (FCPE)

When you make a contribution, you can choose from several investment options available within your PEE.

You’re free to allocate your savings among these options as you wish, and you can change your investment choices online at any time, free of charge.

How to choose the right FCPE for you

Taxation

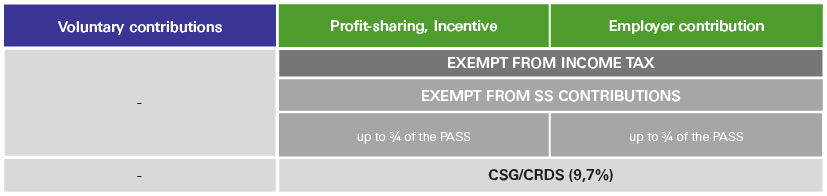

At the time of contribution

- Individuals registered as tax residents outside France are exempt from CSG and CRDS if they are not covered by a mandatory French health insurance scheme.

- PASS: Annual Social Security ceiling, i.e. €48 060.00 for 2026/IT: income tax

Source: HSBC Asset Management, January 2026. For illustrative purposes only.

Please note:

- Your employer covers your account-keeping charges.

- Your voluntary contributions are limited to 25% of your gross annual income (all employee savings plans combined)

At withdrawal

The savings are locked in for five years, but there are several reasons that allow you to access them early, such as marriage or entering into a civil partnership, termination of your employment contract, and others.

At maturity, you are free to choose whether to withdraw all or part of your savings as a lump sum, or to keep all or part of your assets within the plan.

ps:social security contribution

Source: HSBC Asset Management, January 2026. For illustrative purposes only.

Calculation of capital gains

Capital gains are determined using a Weighted Average Acquisition Price (PMPA), which represents the weighted average of the various purchase prices of the securities. The difference between the sale price and the PMPA indicates the individual capital gain or loss realized.

Capital gains are calculated in tiers, taking into account historical social contribution rates, which have increased over time. The portion of capital gains accrued or realized on contributions made during different periods is subject to the respective rates. This calculation method applies to income from amounts paid before 1 January 2018. It remains in effect if the PERCO is transferred or converted into a PERE-CO before 1 January 2023.

Social security contributions are deducted by Natixis Interepargne when your savings are paid out and are remitted directly to the tax authorities.