The PERCOL – Collective company retirement savings plan

Are you looking to build up savings and/or finance your projects with support from your company?

Whether it’s purchasing your main residence, carrying out renovations, or simply setting money aside to better prepare for retirement either as a lump sum or an annuity

The PERCOL allows you to fund these goals under favourable conditions.

The advantages of PERCOL

The advantages of PERCOL

|

An additional source of income for your retirement |

|

|

You can save time (unused leave days) |

|

|

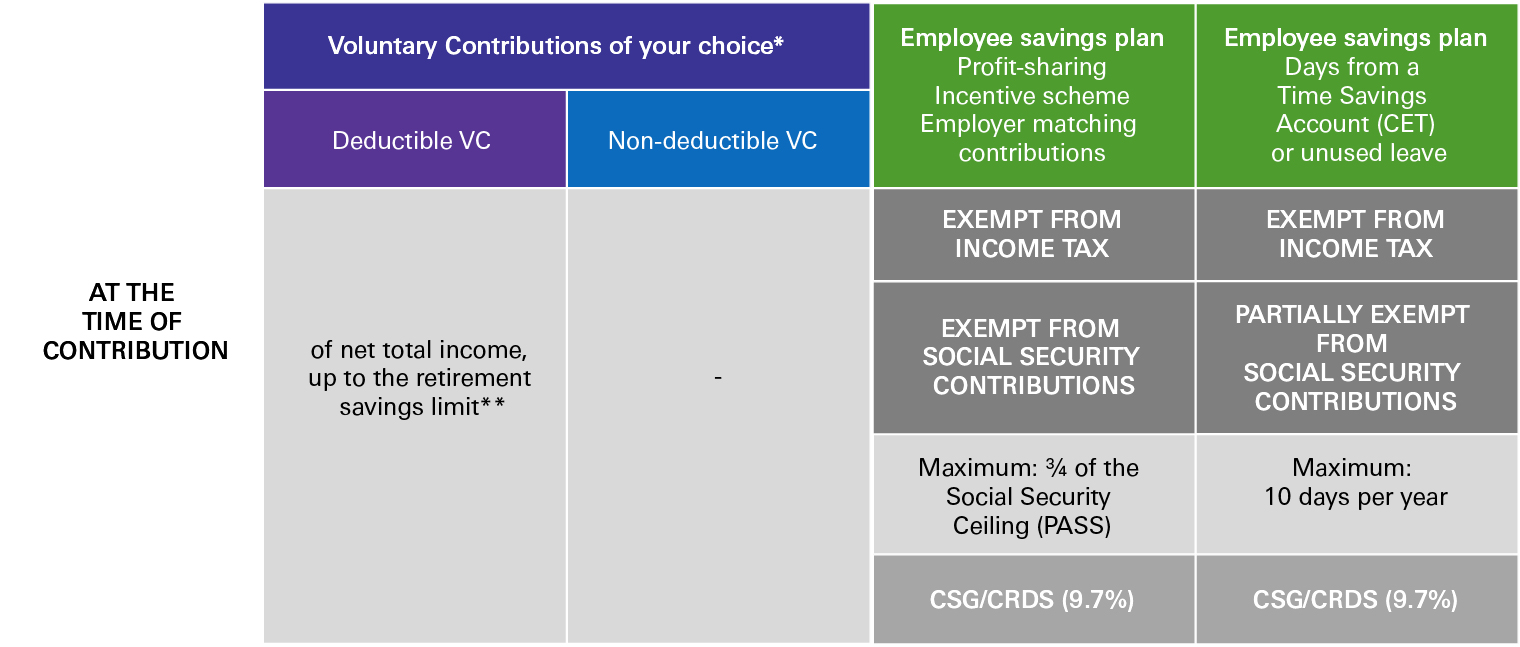

Your annual voluntary contributions are not capped; however, if you choose to make tax-deductible voluntary contributions, these are limited to your personal retirement savings cap |

|

|

Did you know? |

|

|

|

PERCOL: A savings tool for everyone

To access a Collective company pension plan (PERCOL), certain conditions must be met::

- the plan must be set up by your employer

- a length-of-service requirement for employees, which cannot exceed three months

Please note that joining the PERCOL is optional for employees.

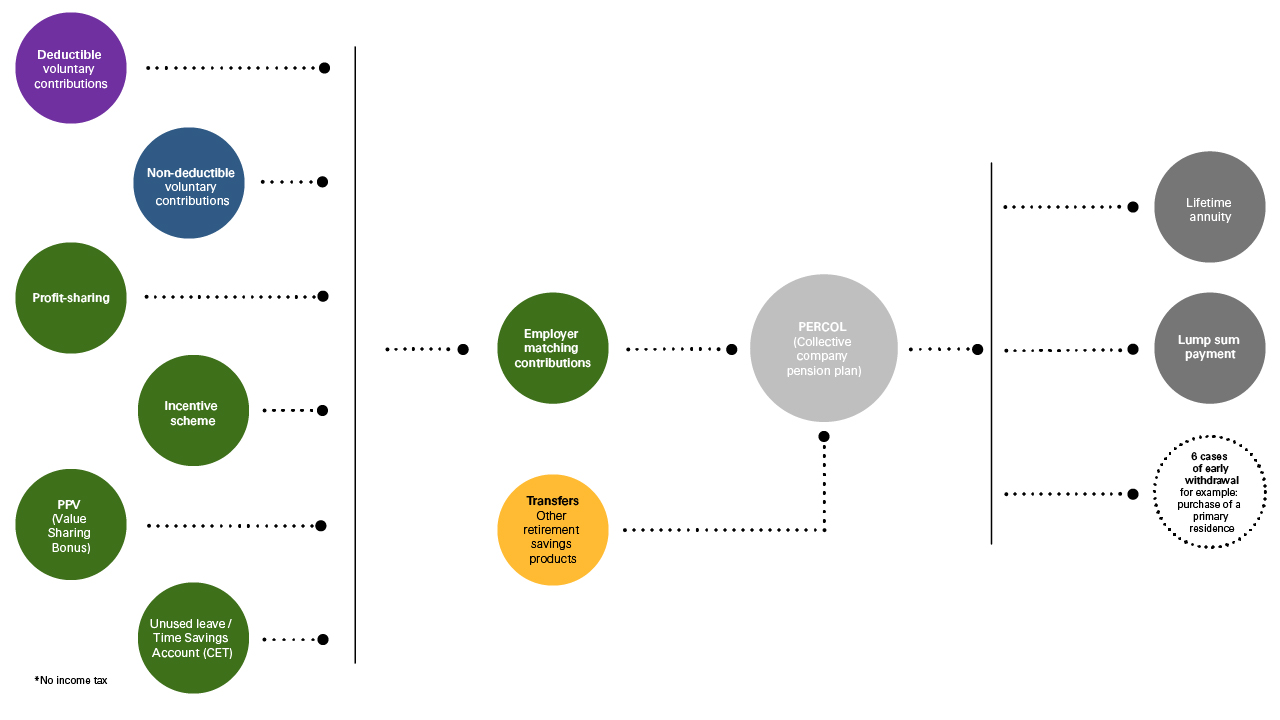

Sources of funding

You can fund your plan with:

- voluntary contributions, which you may choose to deduct from your total net income for income tax purposes,

- contributions made by your employer: profit-sharing, incentive bonuses, and matching contributions, according to the agreements in place within your company,

- time (days recorded in a Time Savings Account [CET], or if not available, unused RTT days, paid leave days beyond the fourth week, etc.),

- the transfer of previous retirement savings products such as Article 83, PERP, PERCO, etc.) under certain conditions

Accessing your savings

Before retirement

Early withdrawal is permitted in the following cases

- purchasing or building your primary residence (except for amounts contributed through mandatory contributions)

- termination of self-employment due to court-ordered liquidation

At the legal retirement age or upon retiremente

The account holder can choose to access their savings:

- as a lump sum, either in a single payment, in installments, or as a lifetime annuity,

- as a combination of lump sum and annuity.

Learn more about early withdrawal options

Investing my retirement savings

The PERCOL plan offers two types of management:

Self-directed management

- This option allows employees to freely choose their investments based on their personal situation, investment horizon, and risk tolerance.

- Employees can allocate their savings among different investment options and adjust their choices at any time.

- The PERCOL plan offers at least three investment options with different risk profiles, including at least one solidarity-based FCPE fund. Except for the solidarity-based FCPE, eligible FCPEs within PERCOL may hold up to 10% in unlisted securities and up to 10% in shares of the company or related companies (Article L.3344-1 of the French Labour Code).

- To better understand their risk tolerance, employees can determine their investor profile using the simulator at www.epargne-salariale-retraite.hsbc.fr/en/epargnants/simulateurs.

- HSBC offers a wide range of FCPE fundsacross all asset classes, with broad geographic coverage and specific investment themes.

Guided management

- Guided management within the PERCOL plan involves a predefined and evolving allocation over time, designed to grow the investor’s capital for retirement while protecting their savings through a gradual reduction of market risk

- This approach allows employees to delegate the financial management of their savings.

- Employees can combine guided management with self-directed management, and they can switch between the two at any time, transferring their assets as they wish

There are two main approaches:

Guided management by horizon:

- Savings are invested in a single fund that matches the chosen investment horizon or risk profile. The asset allocation within this fund will evolve over time.

Guided Management by grid:

- Employees’ savings are invested across several funds, each aligned with the selected investment horizon or risk profile. The allocation between these funds is automatically adjusted over time through rebalancing among the chosen FCPEs.

Taxation of the PERCOL plan

Taxation of the PERCOL plan

The Collective Company PER (PERCOL) is made up of different compartments, which are determined by the origin of the amounts contributed or transferred, as well as the type of management chosen for your investment options (self-directed or guided management).

Your savings are therefore allocated according to the source of your assets.

For example: The employee savings compartment receives amounts from profit-sharing/incentive schemes, time savings, and any employer matching contributions.

Each compartment (deductible contributions, non-deductible contributions, employee savings, mandatory contributions) is subject to its own specific tax treatment.

At the time of contribution

*By default, voluntary contributions are tax-deductible.

** To determine the maximum amount each saver can deduct, refer to the available tax allowance shown on your most recent income tax notice. Note that if you file a joint tax return, you can use your spouse’s unused allowance.

The retirement savings cap is reduced by certain contributions, such as mandatory contributions paid into an Article 83 or PER, employer matching, and days saved in a PERCO or PER.

- Amounts paid into the plan / IR: income tax / VV: voluntary contributions

Source: HSBC Asset Management. February 2026. For illustrative purposes only

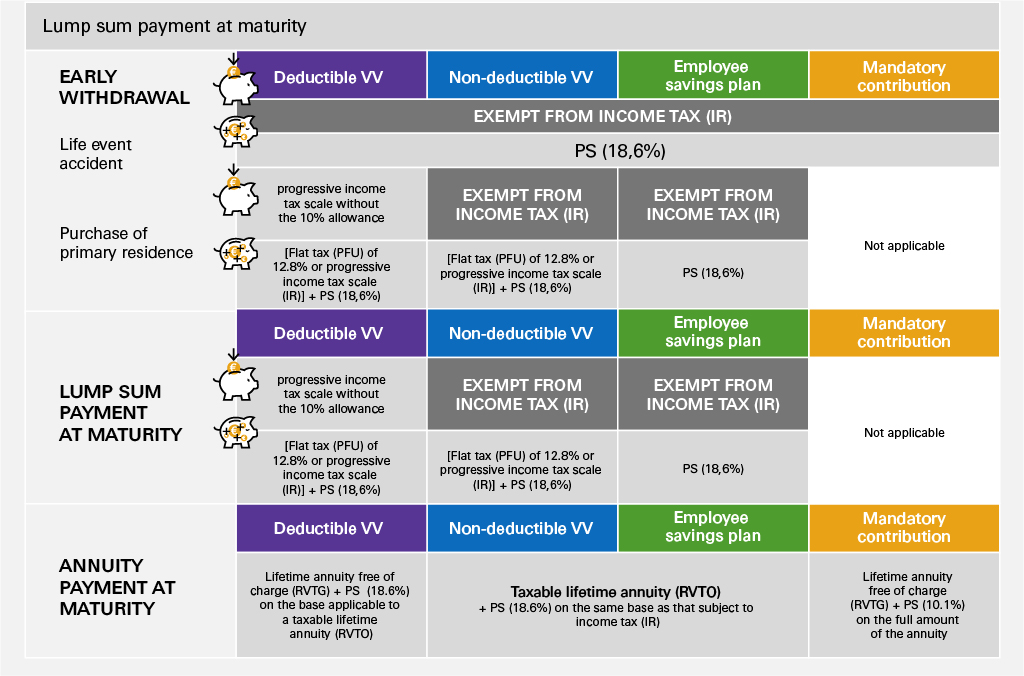

At withdrawal

Lump-sum payment at maturity

|

|

IR: Income tax / PS: Social contributions / VV: Voluntary contributions / PFU: Flat tax of 12.8%, for a total rate of 30% (including 18.6% social contributions). RVTO: Annuity taxed at the progressive income tax scale on a portion of its amount, determined by the beneficiary’s age when the annuity begins RVTG: Annuity taxed as a retirement pension under the progressive income tax scale, after a 10% allowance is applied |

*Employee savings : Profit-sharing, Incentive bonuses, Employer matching contributions, Days from a Time Savings Account (CET), or unused leave days

**Mandatory contributions : amounts transferred only from an Article 83 plan or a Mandatory PER

- Source: HSBC Asset Management. February 2026. For illustrative purposes only.