The mandatory PER – PERO

Would you like to build up savings and/or finance your projects with support from your company?

Whether it’s purchasing your primary residence, carrying out renovations, or simply setting money aside to better prepare for retirement, either as a lump sum or an annuity.

The PERO allows you to finance these goals under favourable conditions.

The advantages of the mandatory PER

The advantages of the mandatory PER

|

An additional source of income for your retirement |

|

|

Access to AXA’s euro-denominated fund: a turnkey management solution that ensures a balance between returns and security as you approach retirement. |

|

|

Tax benefits related to the deductibility of voluntary contributions (within the limits of current legal thresholds) and the insurance wrapper for asset transfers. |

|

|

Did you know? |

|

|

|

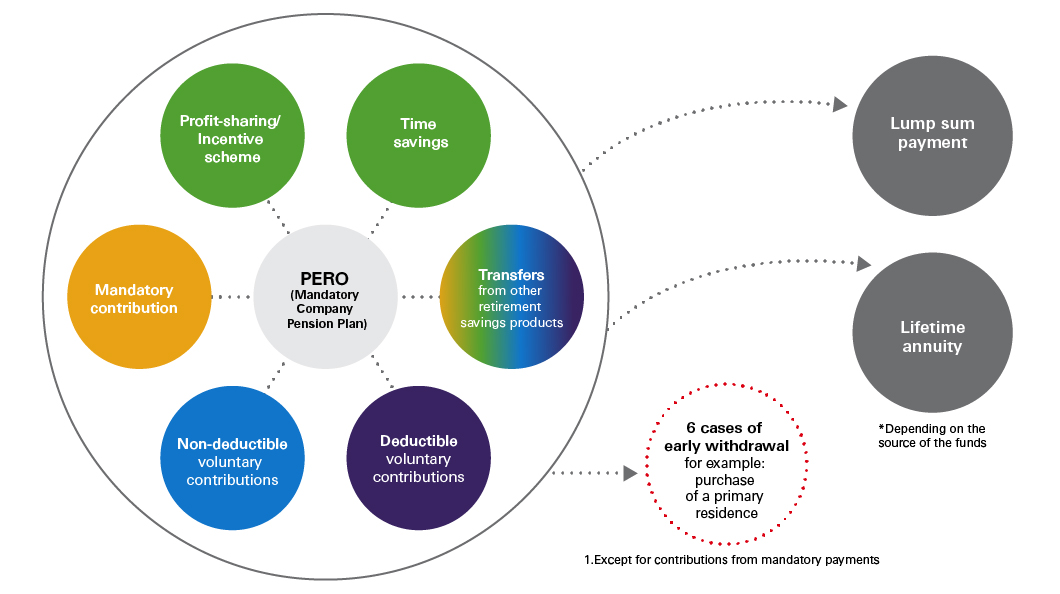

PERO: A savings tool for everyone

To be eligible for a Mandatory Retirement Savings Plan (PERO), certain conditions must be met:

- the plan must be set up by your employer

- for employees, a length-of-service requirement may apply, but it cannot exceed 12 months

Please note that employee participation in the PERO is mandatory. All employees who meet the objective criteria established by the company will be included in the compulsory contributions, except in specific cases.

Sources of funding

You can fund your plan with:

- voluntary contributions ;

- bonuses paid by your employer: profit-sharing and incentive payments, depending on the agreements in place within your company;

- time (days credited to a Time Savings Account, or if not available, unused leave such as RTT days or paid leave beyond the fourth week, etc.).

Accessing your savings

Before retirement

Early withdrawal is permitted in the following cases

- life events (accidents or hardships)

- purchasing your primary residence (applies to voluntary contributions and employee savings)

At the legal retirement age or upon retirement

The account holder can choose to access their savings:

- to amounts from compulsory contributions*

- for all other components, you can choose between a lump-sum payment and/or an annuity

*Savings from compulsory contributions will be paid out as a lump sum if the gross annual annuity is less than €1,320.

https://www.epargne-salariale-retraite.hsbc.fr/en/epargnants/debloquer-son-epargne

Investing my retirement savings

The PERO offers two types of management options:

Self-directed management

- You have the freedom to choose your investments based on your personal situation, investment horizon, and risk tolerance.

- You can allocate your savings among the various investment options offered and adjust your choices at any time.

- To assess your risk profile, you can use the investor profile simulator:

www.epargne-salariale-retraite.hsbc.fr/en/epargnants/simulateurs - In addition to FCPE funds, you can also invest in a euro-denominated fund offered by our partner AXA.

Guided management by allocation grid

- The guided management of the PERO is based on a predefined and evolving allocation strategy. Its goal is to grow your capital for retirement while protecting your savings through a gradual reduction of market risk over time.

- This approach allows you to delegate investment decisions to the PERO manager.

- Your savings are invested across several options, depending on your chosen investment horizon. The allocation between each FCPE and the euro fund will automatically adjust over time through rebalancing between the selected investment vehicles.

- You can combine guided management with self-directed management, and you always have the flexibility to switch from guided to self-directed management, or vice versa, at any time.”

Taxation of the Mandatory PER

The Mandatory PER is made up of different compartments, depending on the source of the amounts paid in or transferred, as well as the type of management you choose for your investments (self-directed or guided management).

Your savings are therefore allocated according to the origin of your funds.

For example:

- The employee savings compartment receives amounts from profit-sharing, incentive payments, and time savings.

- The compulsory contributions compartment receives mandatory contributions from the company and/or employees.

Each compartment (tax-deductible contributions, non-deductible contributions, employee savings, compulsory contributions) is subject to its own specific tax treatment.

At the time of contribution

|

Mandatory contribution |

Employer contribution : |

| Exempt from income tax 1 Exempt from social security contributions 2 |

Employee contribution : |

| Deductible from taxable salary 1 Subject to social security contributions (salary) |

CSG/CRDS (9,7 %) |

![]() Exemptions and deductibility within regulatory limits

Exemptions and deductibility within regulatory limits

(1) within the limit* of 8% of the employee’s gross annual salary, capped at 8 times the Social Security Ceiling (PASS)

(2) within the limit* of:

- 5% of the PASS, or

- 5% of the gross annual salary, up to a maximum of 5 times the PASS.

*these limits are reduced by any employer matching contributions to a PERCO or Collective PER.”

Voluntary contributions of your choice

| Deductible voluntary contributions (applied by default) | Non-deductible voluntary contributions |

|---|---|

| Deductible from net total income, up to the individual retirement savings limit 3 | - |

![]() To determine the maximum amount each saver can deduct, refer to the available tax allowance shown on your most recent income tax notice. Please note that if you file a joint tax return, you can also use your spouse’s unused allowance.

To determine the maximum amount each saver can deduct, refer to the available tax allowance shown on your most recent income tax notice. Please note that if you file a joint tax return, you can also use your spouse’s unused allowance.

(3) the maximum is the higher of 10% of taxable professional income, limited to 8 times the PASS, or 10% of the PASS.

This tax envelope is also used for deductible voluntary contributions made to other retirement savings plans (PER, Article 83, PERP, Préfon, etc.). The envelope is reduced by compulsory contributions, saved days, and/or employer matching paid into a retirement savings plan.

| Profit-sharing, Incentive scheme * | Days from a Time Savings Account (CET) or, if not available, unused leave days |

|---|---|

| Exemption from income tax | Exemption from income tax |

| Exemption from social security contributions - Maximum: ¾ of the Social Security Ceiling (PASS) | Partial exemption from social security contributions - Maximum: 10 days per year |

| CSG/ CRDS (9,7%) |

CSG/CRDS (9,7 %) |

![]() *If a PER is available to all employees within the company

*If a PER is available to all employees within the company

At withdrawal

Lump-sum payment at maturity

| Deductible voluntary contributions | Non-deductible voluntary contributions | Employee savings plan | |

|---|---|---|---|

| Invested amounts (Capital) |

progressive income tax scale without the 10% allowance | Exemption from income tax | Exemption from income tax |

| Capital gains | [Flat tax (PFU) of 12.8% or progressive income tax scale (IR)] + PS (18,6%) | [Flat tax (PFU) of 12.8% or progressive income tax scale (IR)] + PS (18,6%) | PS (18,6 %) |

Annuity payment at maturity

| Deductible voluntary contributions |

Non-deductible voluntary contributions | Employee savings plan | Mandatory contribution |

|---|---|---|---|

| Lifetime annuity free of charge (RVTG) + PS (18.6%) on the base applicable to a taxable lifetime annuity (RVTO) | Taxable lifetime annuity (RVTO) + PS (18.6%) on the same base as that subject to income tax (IR | Taxable lifetime annuity (RVTO) + PS (18.6%) on the same base as that subject to income tax (IR | Lifetime annuity free of charge (RVTG) + PS (10.1%) on the full amount of the annuity |

Early withdrawal

| Life event accident (5 cases) | Deductible voluntary contributions | Non-deductible voluntary contributions | Employee savings plan | Mandatory contribution |

|---|---|---|---|---|

| Invested amounts (Capital) |

Exemption from income tax | Exemption from income tax | Exemption from income tax | Exemption from income tax |

| Capital gains | PS (18,6 %) | PS (18,6 %) | PS (18,6 %) | PS (18,6 %) |

| Purchase of primary residence | Deductible voluntary contributions | Non-deductible voluntary contributions | Employee savings plan |

|---|---|---|---|

| Invested amounts (Capital) |

progressive income tax scale without the 10% allowance | Exemption from income tax | Exemption from income tax |

| Capital gainss | [Flat tax (PFU) of 12.8% or progressive income tax scale (IR)] + PS (18,6%) | [Flat tax (PFU) of 12.8% or progressive income tax scale (IR)] + PS (18,6%) | PS (18,6 %) |

Employee Savings: Profit-sharing, Incentive payments, Value-sharing bonus, Days from a time savings account (CET), or unused leave days IR: Income tax / PS: Social security contributions / PFU: Flat tax of 12.8%, for a total rate of 31.4% (including 18.6% social contributions). RTVO: Annuity taxed at the progressive income tax scale on a portion of its amount, determined by the beneficiary’s age when the annuity begins. RTVG: Annuity taxed as a retirement pension at the progressive income tax scale, after a 10% allowance.

The HSBC Mandatory PER is an insurance-based PER, so it benefits from the inheritance tax advantages associated with life insurance.